What Is an ICHRA, And Is It Right For Your Small Business team’s Benefits?

If you've been trying to offer health benefits to your employees but keep running into the same wall— the premiums are too high, the plans don't fit everyone's needs, or you simply can't afford to commit to a fixed group plan— there's a newer option that a lot of small businesses are starting to pay attention to.

It's called an ICHRA. And even though that acronym might not be the most friendly off the bat, the concept is actually pretty simple once you get to know it. So let’s break down what an ICHRA is, and if it’s the right choice for your small business team’s health insurance benefits!

What Is an ICHRA?

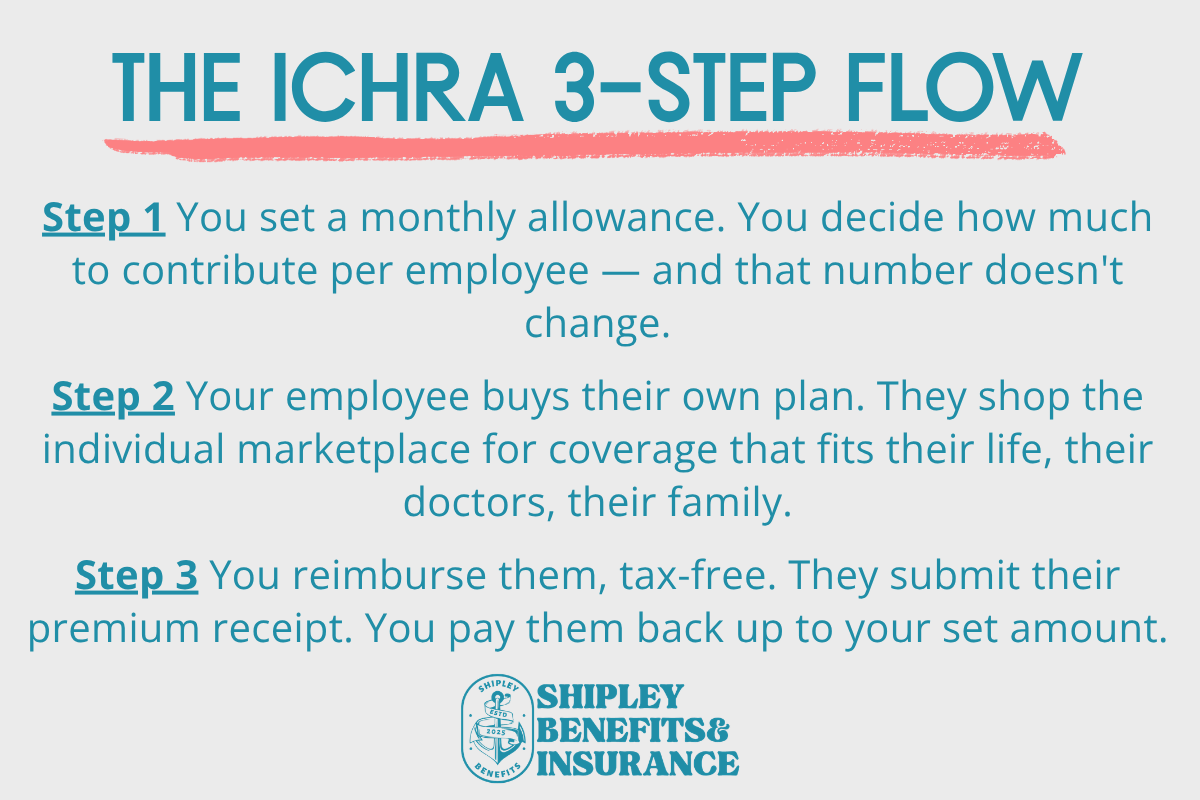

ICHRA stands for Individual Coverage Health Reimbursement Arrangement. It's a formal way of saying: you, the employer, give each employee a set monthly dollar amount, and they use that money to buy their own individual health insurance plan.

Instead of picking one group plan and hoping it works for your whole team, you define the budget. Your employees shop for the plan that actually fits their life. That includes their doctors, their family size, their budget, and their preferences. You reimburse them up to your set allowance, tax-free. That's it.

It's a defined contribution model, which means you know exactly what you're spending every month. No more opening a renewal letter and discovering your premiums jumped 20%.

Why Is Everyone Talking About ICHRAs Right Now?

Because the traditional group health insurance model is becoming harder and harder to sustain for many small businesses. Premiums for small group plans have increased around 11% in 2026, and for very small groups (think two to five employees), and costs have climbed even faster. When you're a small business operating on a real budget, that kind of unpredictability is genuinely painful.

An ICHRA solves the cost-predictability problem. You set your contribution amount, and that number doesn't change unless you decide to change it. The premium volatility of the individual market doesn't land on your plate the same way. It's your employees who are choosing and managing their own plans.

There are real trade-offs to that, which I'll get to in a moment. But that's the core appeal.

Who Can Offer an ICHRA?

Any employer, regardless of size, can offer an ICHRA. That includes sole proprietors who want to cover themselves, very small businesses with just a handful of employees, and growing companies that want a flexible benefits structure as they scale.

There are no minimum or maximum employee count requirements to offer an ICHRA. You can set different allowance amounts for different employee classes (for example, full-time versus part-time employees, or employees in different states) as long as you follow the rules around how those classes are defined.

What Can Employees Use the Reimbursement For?

To receive tax-free reimbursement through an ICHRA, employees must be enrolled in a qualifying individual health insurance plan. This can include plans purchased on the ACA Marketplace, off-exchange individual plans, and, in some cases, Medicare. Employees submit their premium receipts, and you reimburse them up to your set monthly allowance.

Most ICHRA platforms also allow reimbursements for qualified medical expenses beyond just premiums— things like copays, deductibles, and certain out-of-pocket costs, depending on how you set up the plan.

What Are the Real Trade-Offs?

I want to be straightforward here, because I think it's important that small business owners go into any benefits decision with a clear picture.

ICHRAs work really well when the individual insurance market is stable, and your allowance is generous enough to cover a meaningful plan. In 2026, that's a more complicated picture than it was a few years ago. ACA premiums rose significantly this year after enhanced subsidies expired at the end of 2025, which means that in some markets, the individual plans your employees would be choosing from are more expensive than they used to be.

If your ICHRA allowance doesn't keep pace with what a reasonable plan actually costs in your employees' area, they may end up choosing a high-deductible bronze plan just to keep their out-of-pocket premium manageable. That's not necessarily a bad thing, but it's worth understanding before you set your allowance amounts.

The other consideration is administrative. Traditional group plans come with a lot of employer-side management already handled. With an ICHRA, employees are shopping on their own, and they'll have questions. Making sure your team has the support and resources they need to make good decisions is part of running this kind of benefit well.

Is an ICHRA Right for Your Business?

Honestly, it depends. For some small businesses— especially those with employees in different states, part-time teams, or highly variable staffing— an ICHRA can be a genuinely elegant solution. For others, a traditional small group plan or a QSEHRA (a similar reimbursement arrangement designed specifically for businesses with fewer than 50 employees) might be a better fit.

What I've found working with small business owners is that most people have never had anyone sit down and walk them through the comparison. They hear "ICHRA" and assume it's too complicated, or they assume their only option is a group plan because that's what they've always known.

You have more options than you think. And figuring out which one actually fits your situation— your team size, your budget, your state, your goals— is exactly the kind of conversation I love having.

If you've been wondering whether there's a smarter way to handle benefits for your team, let's talk. No pressure, no call center. I’d love to set up a real conversation about what might actually make sense for you.

Shipley Benefits & Insurance specializes in employee benefits and insurance solutions for small businesses and individuals. We help you understand your options in plain language so you can make decisions you feel confident about.

“I'm a business owner, and the level of service Kate has provided on an individual policy has already made the decision for me — when my company grows to the point of needing a group health or benefits policy, Shipley Benefits is my first and only call. That kind of trust isn't built by selling a plan. It's built by showing up after the sale, consistently, when things get complicated.

Kate runs a small, independent operation and delivers the kind of service that large brokerages market but rarely execute. If you are self-employed or run a small business and need someone who will actually advocate for you when the insurance system makes it difficult, Kate is that person.

And let's be honest. When does the insurance system ever make it easy? Have someone on your side who knows the system and who will provide real guidance.”— Chad L. on Google