Tax Season 2026: What Small Business Owners Can Deduct (And Most Don't Know About)

Tax season has a way of making everything feel urgent. But here's some good news, especially if you've been sticker-shocked by your 2026 health insurance premiums: the more you're paying for coverage, the more you may be able to deduct.

Whether you're a solo entrepreneur, a small business owner offering group benefits, or somewhere in between, there are deductions available to you right now that most business owners overlook, misapply, or miss entirely. Let's break them down— clearly, and without the jargon.

1. The Self-Employed Health Insurance Deduction

If you're self-employed and pay for your own health, dental, or long-term care insurance premiums, you may be able to deduct 100% of those costs — directly on your personal tax return, not just as an itemized deduction.

Who qualifies: Sole proprietors, partners, and S-corp shareholders who own more than 2% of the company. You must have a net profit for the year and not be eligible for coverage through a spouse's employer plan.

What it covers: Premiums for health insurance, dental, vision, and qualifying long-term care insurance for you, your spouse, and your dependents.

The big win: This deduction reduces your adjusted gross income (AGI), which can also lower your overall tax bracket — not just your taxable income.

Pro tip: If your premiums went up dramatically in 2026 due to the ACA subsidy cliff, this deduction may offset more than you expect.

2. Group Health Insurance Premiums as a Business Expense

If you offer a group health plan to your employees, the premiums you pay on their behalf are fully deductible as a business expense. This applies to medical, dental, and vision coverage.

What qualifies: Your contributions toward employee premiums under a group health plan. This includes plans purchased directly from insurers or through the SHOP Marketplace.

What doesn't: Your employees' share of premiums (the part deducted from their paychecks) — that's their deduction, not yours.

And don't forget: if you're offering group coverage, you may also be eligible for the Small Business Health Care Tax Credit — worth up to 50% of premiums paid — if you have fewer than 25 full-time equivalent employees with average wages below a certain threshold. This credit often goes unclaimed.

3. QSEHRA and ICHRA Contributions

If you're not offering a traditional group plan but instead reimburse employees for individual health insurance premiums through a Health Reimbursement Arrangement (HRA), those reimbursements are also tax-deductible for your business — and tax-free for your employees.

QSEHRA (Qualified Small Employer HRA): Designed for businesses with fewer than 50 employees that don't offer group coverage. Employers can reimburse employees for individual market premiums and out-of-pocket medical costs up to annual limits set by the IRS.

ICHRA (Individual Coverage HRA): Available to businesses of any size, with no contribution limits. More flexible, but requires employees to be enrolled in individual insurance coverage.

Both arrangements are 100% deductible as a business expense — and they can be a smart alternative to group plans for businesses where a traditional group plan doesn't make financial sense.

4. HSA Contributions — The Double Tax Advantage

If your health plan is paired with a Health Savings Account (HSA), you're sitting on one of the best tax tools available to small business owners.

HSA contributions are tax-deductible when you contribute (even if you don't itemize), tax-free when you use them for qualified medical expenses, and tax-deferred if you invest and let them grow.

For 2026, the IRS contribution limits are $4,300 for individuals and $8,550 for families, with an additional $1,000 catch-up contribution if you're 55 or older.

If you're contributing as an employer to your employees' HSAs, those contributions are also deductible as a business expense — and employees don't pay income tax on them.

5. Dental and Vision Premiums

These often get forgotten in the conversation, but standalone dental and vision insurance premiums are deductible under the same rules as health insurance— both for self-employed individuals and as a business expense for employer-paid premiums.

If you or your team added dental or vision coverage this year, make sure those premiums are included in your deductions.

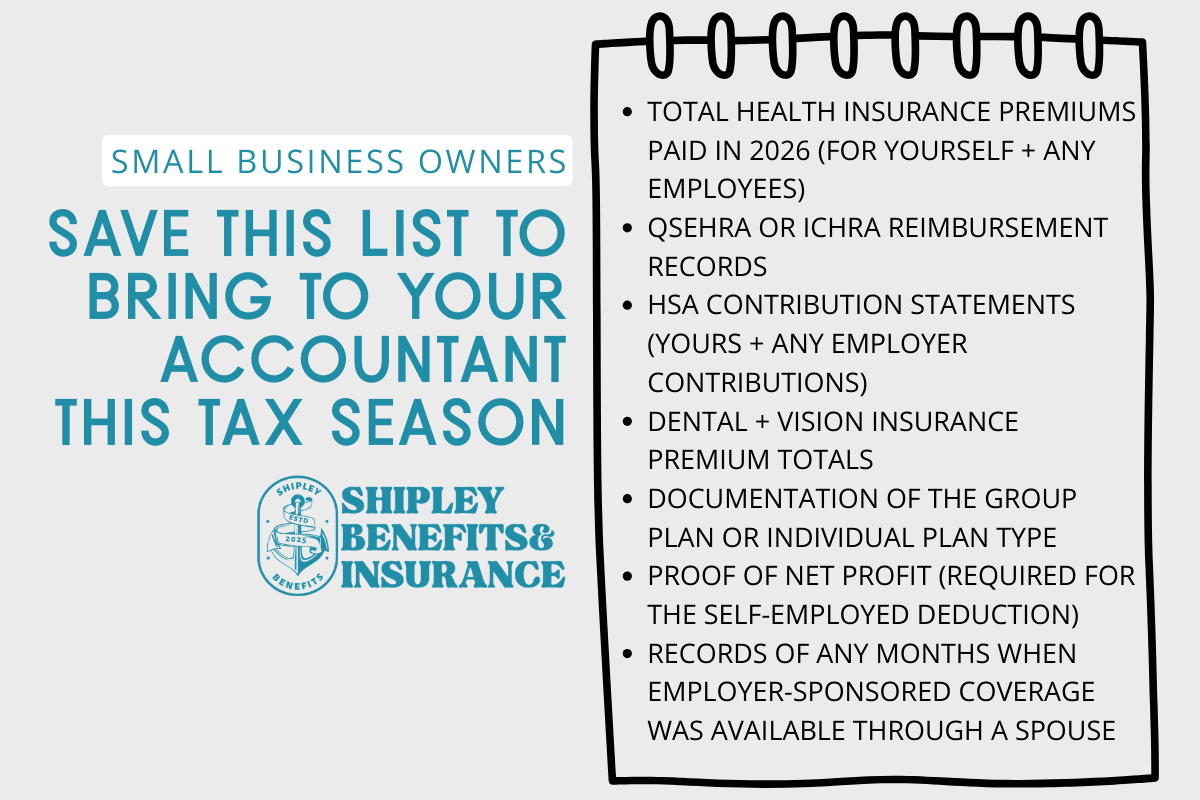

What to Bring to Your Accountant This Tax Season

Save this checklist to pull together before your appointment with your tax professional:

Total health insurance premiums paid in 2026 (for yourself and any employees)

QSEHRA or ICHRA reimbursement records

HSA contribution statements (yours and any employer contributions)

Dental and vision insurance premium totals

Documentation of the group plan or individual plan type

Proof of net profit (required for the self-employed deduction)

Records of any months when employer-sponsored coverage was available through a spouse

The Bottom Line

Yes, most health insurance premiums went up in 2026, some dramatically. But the flip side is that those higher premiums may mean more significant deductions on your tax return. Now is the time to make sure you're capturing every one of them.

Not sure whether your current benefits setup is as tax-efficient as it could be? That's exactly the kind of question we love to dig into. Book a free 30-minute benefits consultation, and let's make sure your 2026 benefits strategy is working as hard for you as you work for your business.

Shipley Benefits & Insurance helps small businesses and individuals in Central Florida and across the country design benefits packages that attract talent, protect families, and make financial sense. Have a question? We'd love to hear from you.

This blog is for informational purposes only and does not constitute tax or legal advice. Please consult your tax professional for guidance specific to your situation.